The latest personal finance tips and insights for Australians at home and abroad

Smart Ways to Spend Your Tax Savings in Australia

The Australian Federal Budget 2024-25 has brought about significant changes, one of the most notable being the confirmation of the long-anticipated Stage 3 Tax Cuts. As an Australian taxpayer, you might be wondering what these changes mean for you and how you can make the most of your newfound tax savings.

This blog is here to help you understand the details of the tax rate changes and provide you with six smart ways to invest your tax savings effectively.

With the right strategies, you can not only boost your financial well-being but also secure a more stable and prosperous future. So, let’s dive into the details of the Stage 3 Tax Cuts and explore how you can put your extra cash to good use.

Section 1: Understanding the Stage 3 Tax Cuts

Overview of Stage 3 Tax Cuts

The Stage 3 Tax Cuts represent a significant shift in Australia’s tax system, aiming to simplify tax brackets and reduce the tax burden on middle and high-income earners. These tax cuts are part of a broader strategy to stimulate economic growth by increasing disposable income, encouraging spending, and promoting investment.

The concept of these tax cuts was first introduced in the 2018 Federal Budget and has since been a topic of much discussion and debate. The goal is to create a flatter tax system with fewer brackets, making it easier for you to understand your tax obligations and potentially giving you more money in your pocket.

Details of Tax Rate Changes

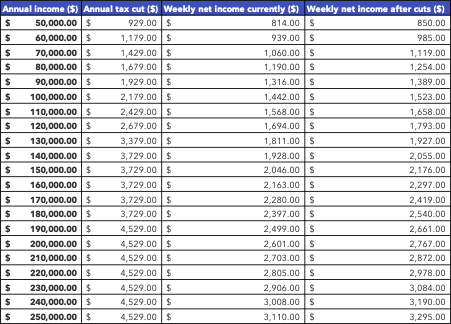

The key changes under the Stage 3 Tax Cuts involve adjustments to the income tax brackets and rates. Here’s a breakdown of the tax savings based on the various income levels.

Figure 1 – Source: Australian Financial Review May 2024

Impact on Australian Taxpayers

The impact of these tax cuts on your finances can be substantial, particularly in terms of the percentage difference up to $190,000 annual income.

Section 2: Smart Ways to Invest Your Tax Savings

1. Pay Down High-Interest Debt

One of the smartest ways to use your tax savings is to pay down high-interest debt. High-interest debt, such as credit card balances and personal loans, can quickly erode your financial stability if left unchecked. By allocating your tax savings towards reducing this debt, you can:

Free Up More Disposable Income: Lowering your debt means fewer monthly payments and less interest accumulation, leaving you with more disposable income each month.

Improve Your Credit Score: Paying off high-interest debt can improve your credit score, making it easier to qualify for loans and get better interest rates in the future.

Gain Financial Peace of Mind: Reducing debt can alleviate financial stress and provide a sense of security, knowing you’re not burdened by high-interest obligations.

2. Boost Your Superannuation Contributions

Another excellent way to invest your tax savings is by boosting your superannuation contributions. Superannuation is a powerful tool for building your retirement nest egg, and making additional contributions can have significant long-term benefits:

Tax Advantages: Contributions to your superannuation fund are generally taxed at a lower rate (15%) compared to your marginal tax rate, providing an immediate tax benefit.

Compounding Interest: The earlier you contribute to your super, the more time your money has to grow through compounding interest, potentially leading to a larger retirement fund.

Secure Your Retirement: By enhancing your superannuation, you’re ensuring a more comfortable and financially secure retirement.

Consider setting up a regular additional contribution to your superannuation fund. Even a small amount added consistently can make a big difference over time.

3. Invest in the Stock Market

Investing in the stock market can be an effective way to grow your wealth, especially with the extra funds from your tax savings. While stock market investments come with risks, they also offer the potential for substantial returns:

Diversify Your Portfolio: Investing in a mix of stocks can help spread risk and increase the potential for returns. Look for a balance between growth stocks, dividend-paying stocks, and defensive stocks.

Long-Term Growth: Historically, the stock market has provided higher returns over the long term compared to other investment vehicles. Patience and a long-term perspective are key.

Professional Advice: Consider seeking advice from a financial advisor to tailor a stock investment strategy that aligns with your risk tolerance and financial goals.

Using your tax savings to build a diversified stock portfolio can set you on the path to achieving your financial objectives, whether it’s saving for a major purchase, funding your children’s education, or planning for retirement.

4. Real Estate Investment

Investing in real estate is a tried and true method for growing wealth and generating passive income. Here’s how you can make the most of your tax savings by diving into the property market:

Rental Income: Purchasing a rental property can provide a steady stream of income. With the right property and tenants, your investment can start paying off almost immediately.

Capital Growth: Real estate typically appreciates over time, offering potential capital gains. Choose properties in areas with strong growth potential and good infrastructure to maximise returns.

Tax Benefits: Property investors can benefit from various tax deductions, including interest on mortgage payments, maintenance costs, and depreciation. These deductions can offset rental income, reducing your overall tax burden.

Portfolio Diversification: Adding real estate to your investment portfolio diversifies your assets, which can help manage risk and enhance returns over time.

Professional Advice: Working with a property investment adviser can be a sensible strategic move to ensure that you’re making the right moves and identifying the right property for you.

If you’re a first-time property investor, consider starting with a smaller, more manageable property. Research the market, evaluate potential rental yields, and consider long-term trends in the area. If you’re expanding your property portfolio, look for properties that complement your existing investments whether this may be a greater focus on capital growth or higher yielding properties.

5. Build an Emergency Fund

An emergency fund is a financial safety net designed to cover unexpected expenses, such as medical emergencies, car repairs, or sudden job loss. Using your tax savings to establish or grow an emergency fund can provide several benefits:

Financial Security: An emergency fund ensures you have the resources to handle unexpected costs without resorting to high-interest debt or disrupting your long-term financial plans.

Peace of Mind: Knowing you have a financial cushion can reduce stress and anxiety, allowing you to focus on other financial goals.

Flexibility: With an emergency fund in place, you have the flexibility to take calculated risks, such as investing in the stock market or real estate, without worrying about immediate financial needs.

Aim to save enough to cover at least three to six months of living expenses. Store your emergency fund in a high-interest savings account or money market fund, where it’s easily accessible but still earns some interest. Avoid investing your emergency fund in stocks or other volatile assets, as you need it to be readily available when emergencies arise.

6. Explore Managed Funds or ETFs

Managed funds and exchange-traded funds (ETFs) are excellent options for investors seeking diversification and professional management without the need to actively manage their investments. Here’s how you can leverage your tax savings by investing in these vehicles:

Diversification: Managed funds and ETFs pool money from multiple investors to purchase a diversified portfolio of assets, spreading risk across various sectors and markets.

Professional Management: These funds are managed by professional portfolio managers who make investment decisions on your behalf, aiming to maximize returns and manage risk.

Cost-Effective: ETFs, in particular, tend to have lower fees compared to actively managed funds, making them a cost-effective way to achieve broad market exposure.

Flexibility: ETFs can be bought and sold on stock exchanges, offering liquidity and flexibility. Managed funds, while typically less liquid, provide access to a wider range of asset classes and investment strategies.

When selecting managed funds or ETFs, consider your investment goals, risk tolerance, and time horizon.

Conclusion

The Stage 3 Tax Cuts confirmed in the Australian Federal Budget 2024-25 present a valuable opportunity for you to enhance your financial situation. By understanding the details of the tax rate changes and strategically investing your tax savings, you can achieve significant financial benefits and long-term security.

To recap, here are six different options to invest your tax savings:

Pay Down High-Interest Debt: Free up disposable income and improve your financial stability.

Boost Your Superannuation Contributions: Secure your retirement with tax-advantaged savings.

Invest in the Stock Market: Diversify and grow your wealth with a long-term perspective.

Real Estate Investment: Generate rental income and benefit from capital growth.

Build an Emergency Fund: Ensure financial security and peace of mind.

Explore Managed Funds or ETFs: Achieve diversification and professional management at a low cost.

Each of these strategies offers unique benefits and can help you make the most of your tax savings. It’s important to tailor your investment approach to your personal financial goals, risk tolerance, and time horizon. Seeking advice from a financial adviser can also help you develop a comprehensive plan that maximises your financial potential.

Remember, the key to successful investing is not just about saving money but making your money work harder for you. By wisely investing your tax savings, you’re taking proactive steps towards a brighter, more secure financial future.

Ally Wealth Management is the trusted ally in finance for Australians at home and across the globe. As both Australian expats and residents, the founders of Ally have a unique understanding of the common personal financial challenges faced.

Book your complimentary appointment with our team at Ally Wealth Management to discuss how we can help you to achieve your financial goals.

Ally Wealth Management Pty Ltd is a Corporate Authorised Representative of Sentry Advice Pty Ltd ABN 77 103 642 888. Sentry Advice holds an Australian Financial Services Licence (AFSL) No. 227 748.

General Advice Warning: The information contained herein is of a general nature only and does not constitute personal advice. You should not act on any recommendation without considering your personal needs, circumstances, and objectives. We recommend you obtain professional financial advice specific to your circumstances.

How Can Employers Better Support Globally Mobile Staff

The modern workforce is increasingly mobile. International assignments, remote work opportunities, and global talent have transformed how businesses operate across…